The pitch deck is open. A friend sent you their term sheet. Your spouse asked what dilution actually means. The capital decision will shape the next decade more than the product decision will.

This page is for the owner who has not yet committed to either path and is reviewing both honestly.

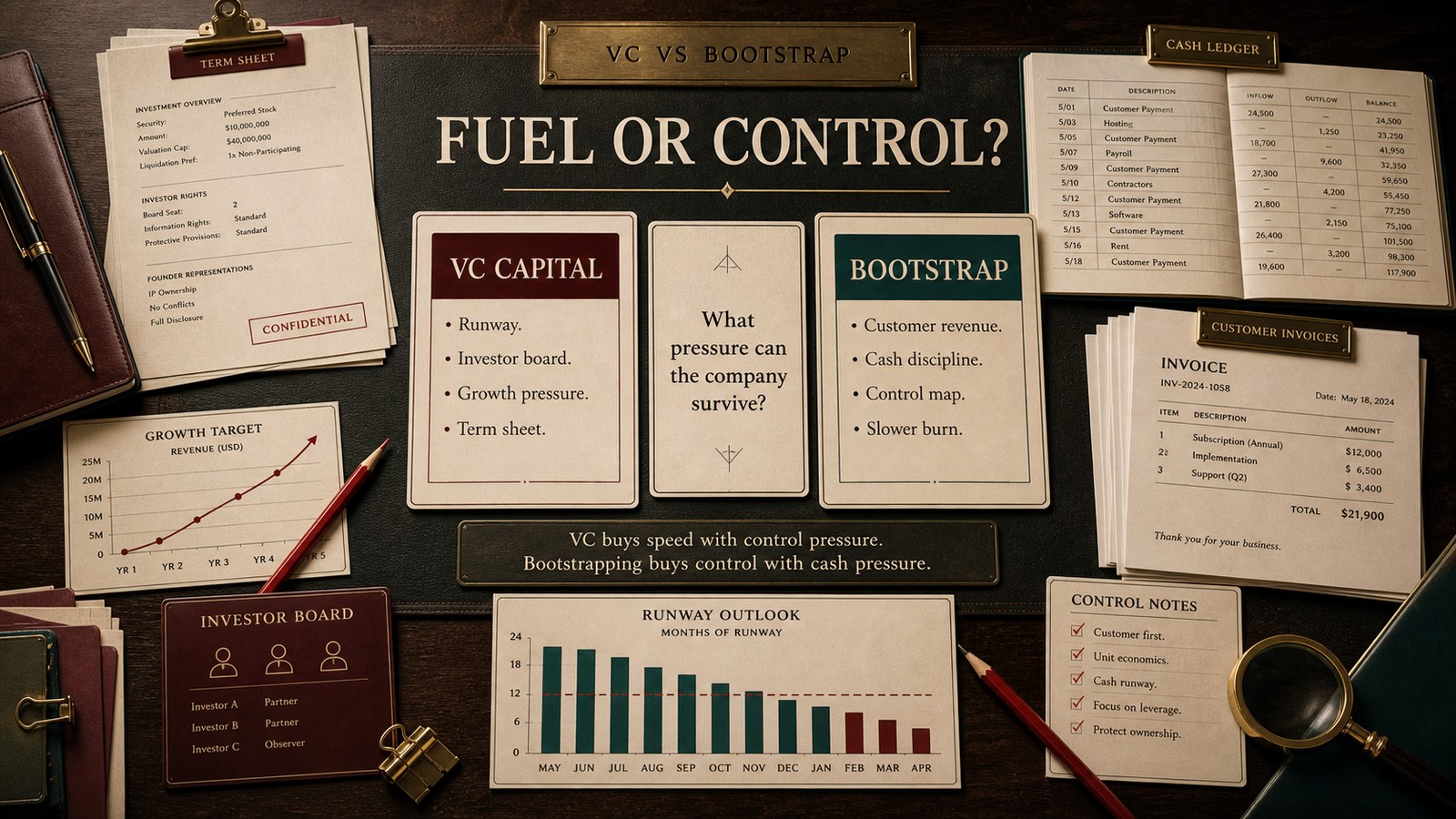

Short answerRaise venture capital when the market window is short, the product needs capital to win, and you are ready to be accountable to a board on a quarterly horizon.

Stay bootstrapped when the window is long, capital-efficiency is achievable, and you want to optimize for control over speed.

The path that fits is not the path that excites you. It is the path that fits the company you are actually building.