Answer

The entity choice is paperwork only until ownership, tax, control, litigation, investment, or exit enters the picture.

The entity choice is paperwork only until ownership, tax, control, litigation, investment, or exit enters the picture.

The whole page in one scan.

The entity choice is paperwork only until ownership, tax, control, litigation, investment, or exit enters the picture.

The founder asks for the best entity. The accountant answers tax. The lawyer answers liability. The investor answers financing. The family answers control.

Ownership intent missing sits under the visible pressure.

Pick the tax answer looks active, but it enters the wrong place.

Use the decision test, then choose the next decision layer.

Entity choice is the decision about how ownership, control, liability, tax treatment, investment path, and exit options are carried by the company structure.

THE FORM IS SMALL. THE CONSEQUENCE IS NOT.

The founder asks for the best entity. The accountant answers tax. The lawyer answers liability. The investor answers financing. The family answers control.

All four may be real. The outlet is the ownership decision underneath the form.

This sits in the ownership and legal structure layer. It is adjacent to tax, family ownership, investor rights, cross-border expansion, and exit planning.

This page does not give legal advice. It gives the decision map to discuss with qualified legal and tax professionals.

Use this business coaching when the entity question is really about ownership, control, tax, investment, liability, or eventual transfer. The boring form suddenly has teeth. Delightful paperwork, if your hobbies include future lawsuits.

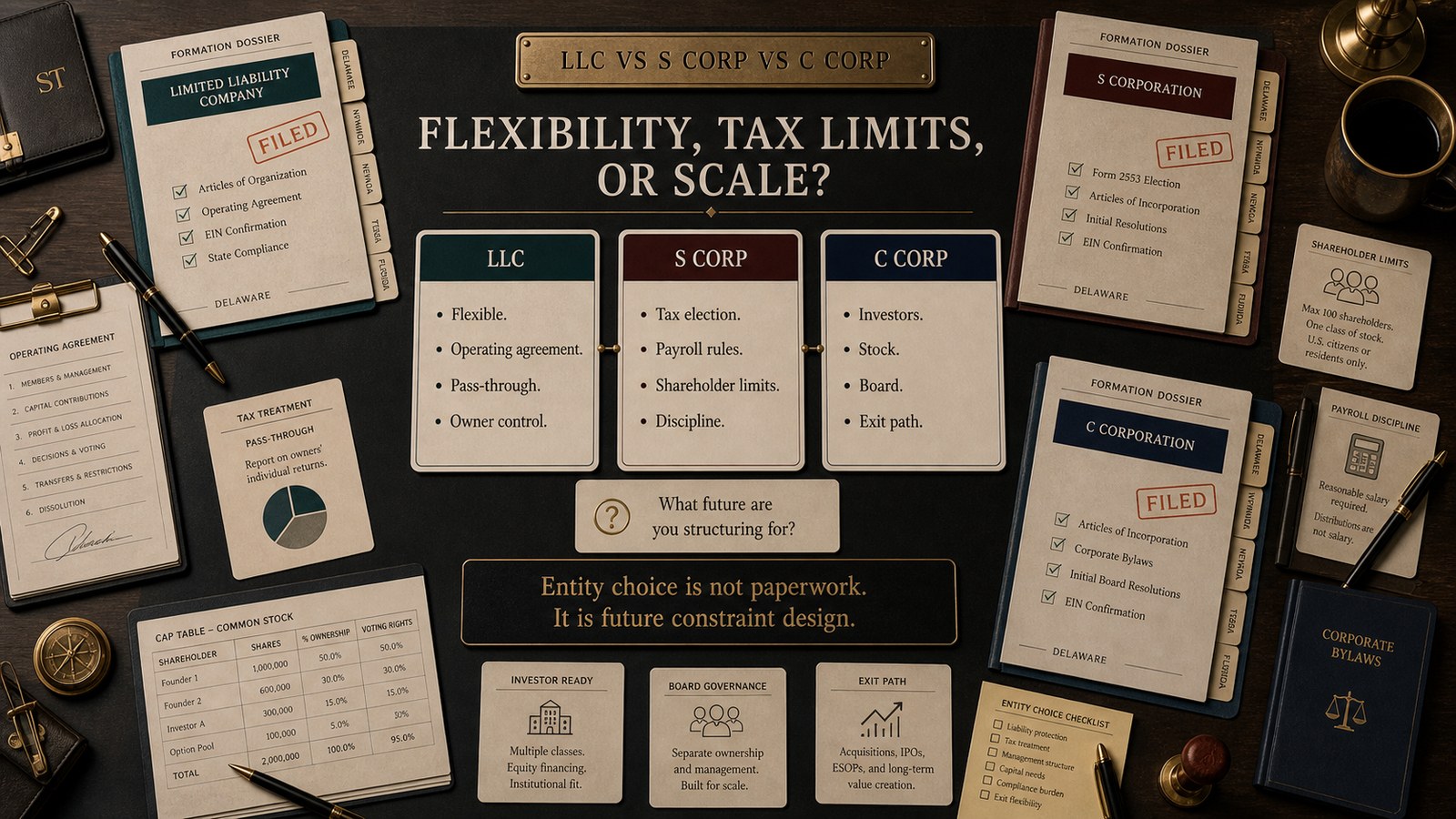

An LLC may fit when flexibility and pass-through treatment matter.

An S Corp election may matter when the facts support it and compliance is clean.

A C Corp may fit when investors, stock, and growth path require it.

The structure should match what the owner may sell, transfer, or protect later.

This is not the first stop when the issue is already plainly legal, tax, regulatory, or cross-border and needs qualified counsel before the Atlas can help frame the business decision.

Ask which entity is best.

Ask what the ownership structure must protect, permit, and survive.

Misuse starts when the buyer treats entity choice as a tax coupon and forgets control, ownership, sale path, and future conflict.

This grid compares the visible signal, the common move, the hidden decision, and the first better move. Scan across each row before choosing the structure.

| Visible signal | Common move | Hidden decision | First move |

|---|---|---|---|

| Tax answer dominates | Pick the lowest tax route | Control and exit are ignored | Map ownership intent first |

| Investor asks for C Corp | Switch immediately | Capital path may not match business reality | Check investor and exit path |

| Family owns pieces informally | Leave it for later | Personal conflict becomes control risk | Document ownership and rights |

| Cross-border sale begins | Assume US form travels | Jurisdiction changes the answer | Add cross-border counsel |

The best entity is not abstract. It is attached to a consequence.

The document waits quietly until life stops being neat.

If the entity creates authority questions, go to governance.

FamilyFamily Business Decision ConflictsIf ownership and family sit together, use the family conflict business coaching.

Cross-borderCross-border business coachingIf countries enter the structure, use the cross-border path.

If three or more questions land as yes, the visible symptom is probably not the whole problem. The decision layer underneath needs to be named before money, software, or authority moves.

Use this page to frame the legal and tax conversation. Go to family dynamics when ownership conflict is personal. Go to cross-border when jurisdiction changes the structure.