Answer first

How to use this

Use this as a filter. If the examples sound familiar, start with the business problem before choosing the fix. If the issue is already expensive, review Business Owner Coaching. If you want the broader problem library, go to Business Problems.

Business owner coaching starts when the obvious fix keeps failing.

Most owners do not need another opinion. They need to know why the same business cost keeps returning after the website, hire, tool, agency, meeting, or strategy push was supposed to solve it.

The problem may be live already. The consequence is real. The owner still has time to choose the next move, but not much time to keep guessing.

The useful question is not, "Can someone give me input?" The useful question is, "Can someone see the pattern I am too close to see and say plainly what must be checked first?"

The category is easy to misunderstand.

A business owner coach is not just a general consultant with a sharper label. A consultant usually improves a function. Sales process. Hiring process. Finance process. Strategy deck. Market research. Those can matter. They are not the same job.

Business coaching is closest to the owner problem. It deals with choices that change the business underneath the visible work: who has authority, what gets funded, whether a partner stays, whether a senior leader is in the wrong seat, whether the board is avoiding the real conflict, or whether the company is being shaped for the next round instead of the next operating chapter.

That is why advisor vs consulting and advisor vs coaching are not word games. They name different jobs. If the question needs execution capacity, hire execution. If it needs emotional processing, find the right care. If it needs business owner coaching, do not bury it under another workstream.

When business owner coaching fits

- 01

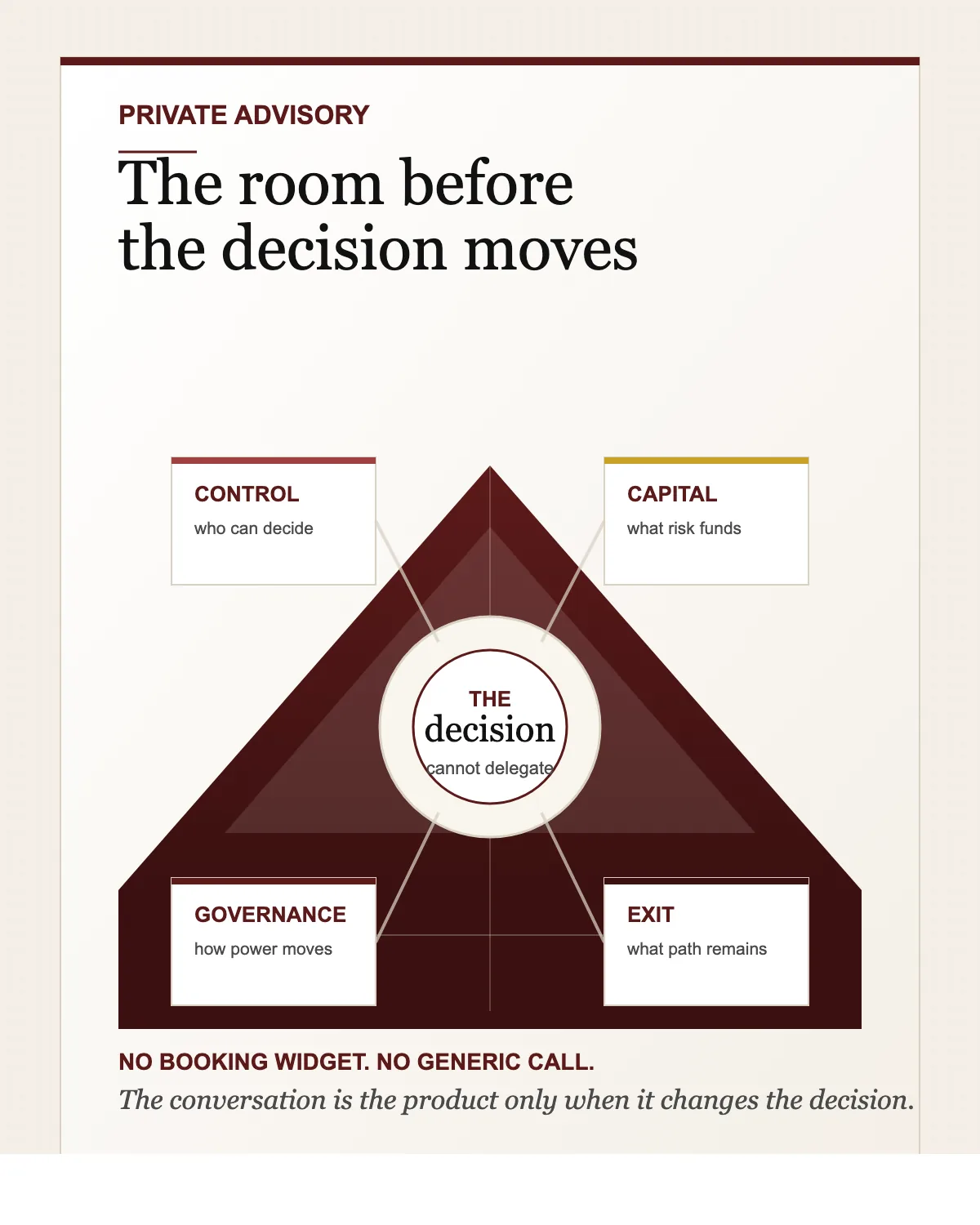

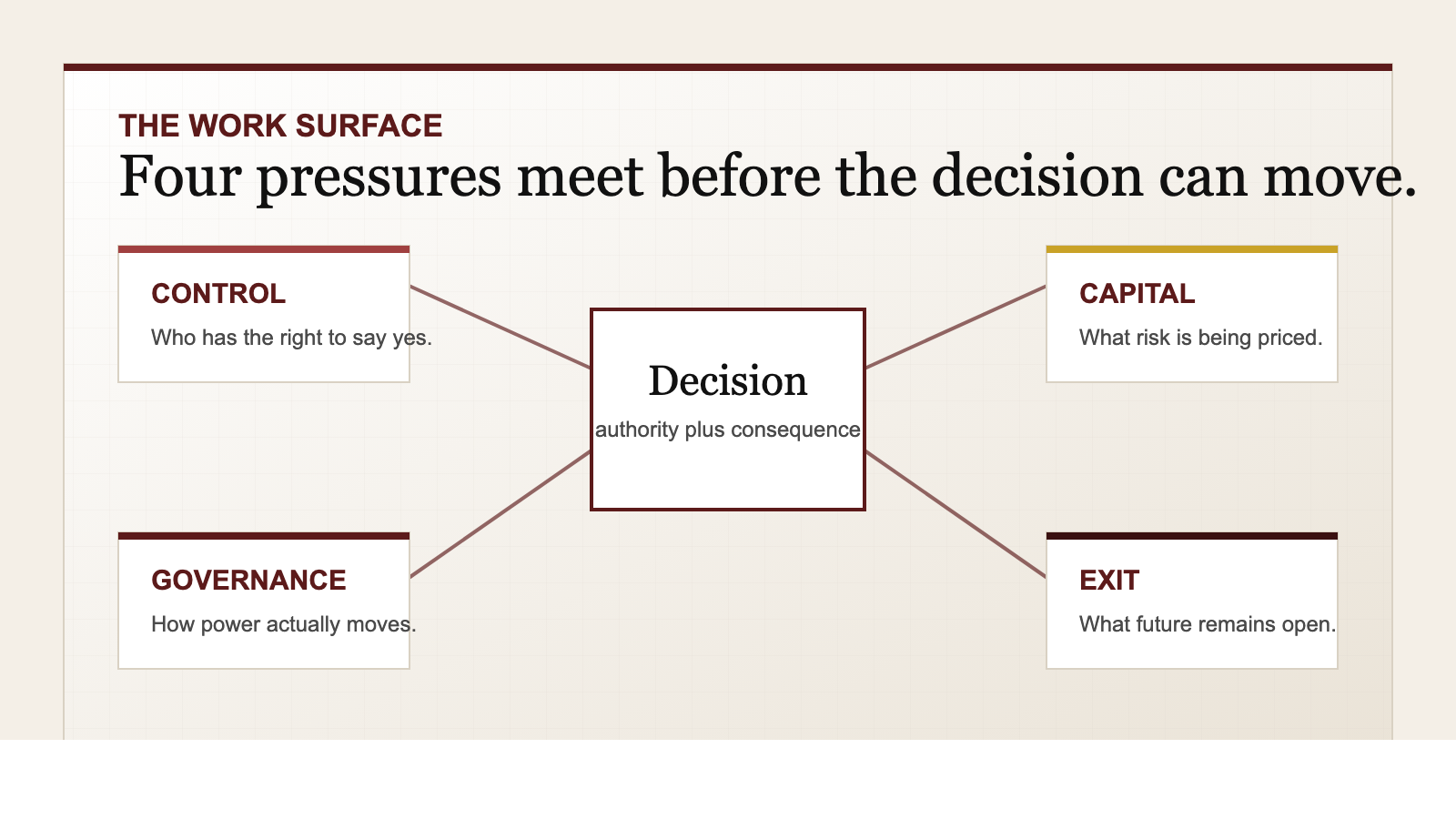

The decision cannot be delegated. If someone else decides, they either lack authority or will carry consequences they do not control.

- 02

The team has too many interpretations. Everyone agrees on the words, but not on what the words mean once money, status, and control enter.

- 03

The company is paying for delay. The cost does not show as one clean invoice. It leaks through hiring, focus, trust, capital timing, and morale.

- 04

The visible problem is not the real problem. The sales issue may be proof. The hiring issue may be authority. The strategy issue may be ownership appetite. The board issue may be consent.

The work is not neutral comfort.

A good business coach should make the team quieter, not more excited. The value is not charisma. The value is precision under pressure.

That means the work often starts by removing false choices. "Should we raise capital?" becomes, "What problem are you trying to solve with capital?" "Should we hire a COO?" becomes, "What authority are you refusing to release?" "Should we take the acquisition offer?" becomes, "Are you selling the company, escaping the next operating chapter, or negotiating from exhaustion?"

If the real problem is not named, the loudest explanation usually becomes the plan. That is expensive.

The decision you avoid does not stay neutral. It starts making smaller decisions for you.

Business owner coaching has boundaries.

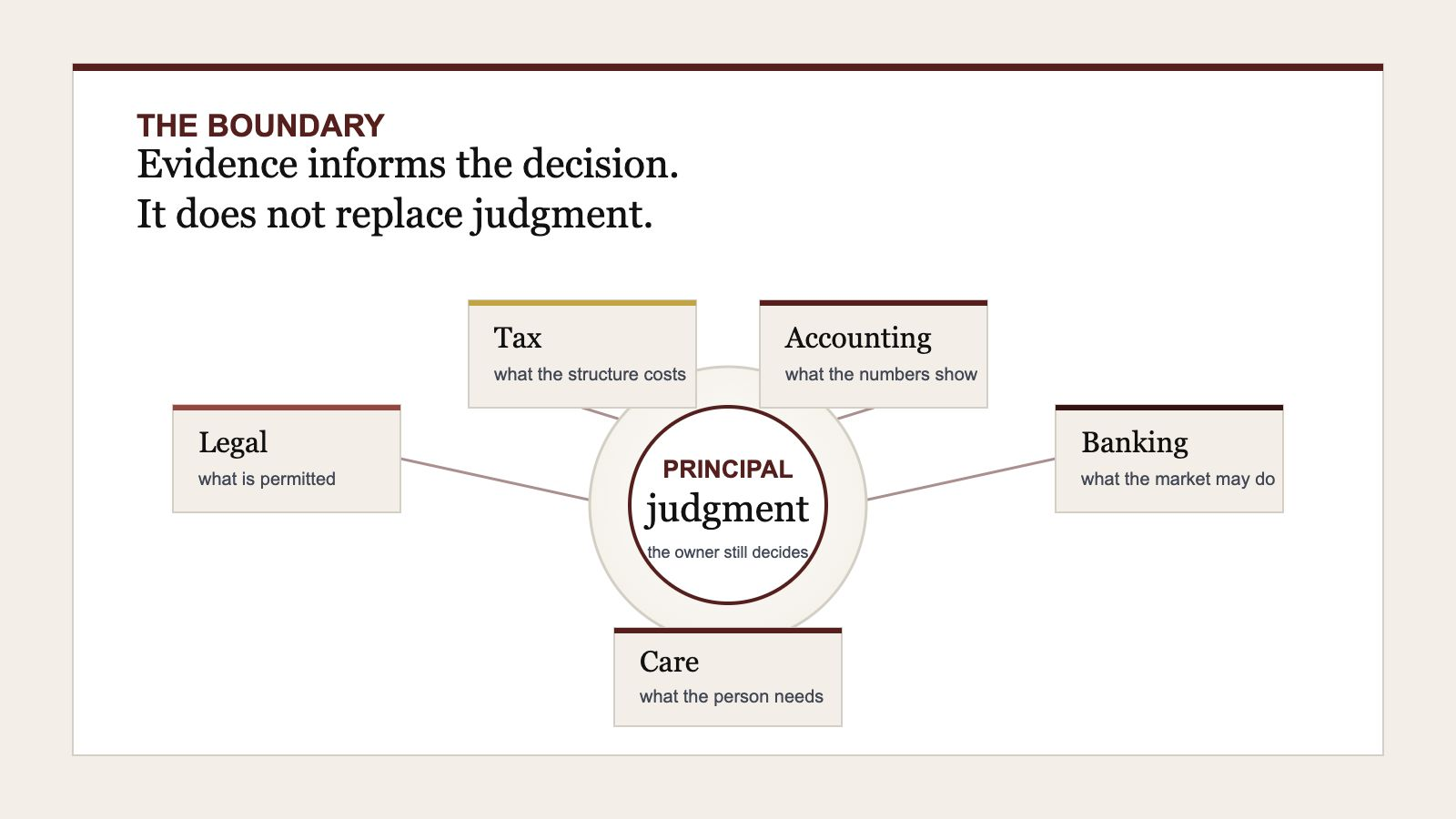

It is not legal advice, tax advice, accounting advice, investment advice, therapy, or a substitute for proper board process. Those boundaries matter. If the primary question belongs to a lawyer, accountant, banker, therapist, or operator, go there first.

Business coaching is useful when those lanes exist but do not settle the business problem. A lawyer can tell you what the agreement permits. An accountant can show what the numbers say. A banker can explain the market. A coach can work on the person. The advisor asks what problem the evidence is actually asking the owner to solve.

On the ground, that distinction saves attention. It stops an owner from turning a structural question into a staffing project. It stops a board from hiding a governance conflict inside a strategy review. It stops a capital decision from becoming a vanity test.

Choose by problem

Unclear problem

Start with the business problem.

For an expensive situation where the owner still does not know the next business move.

Business Owner CoachingOwner constraint

Everything returns to you.

For a business where decisions, approvals, and exceptions keep collecting on the owner.

Owner constraint business coachingBigger project

Question the project first.

For a consulting project, rebuild, hire, or fix that may be aimed at the wrong business category.

Business coaching session vs consulting projectThe useful output is a decision that can move.

Sometimes the output is a yes. Sometimes it is a no. Sometimes it is the uncomfortable discovery that the original question was built to avoid a harder one.

That is still output. A founder who stops solving the wrong business category has already recovered time. A board that names who actually has consent rights can stop pretending alignment exists. An ownership group that sees the real tradeoff can stop buying delay through politeness.

If the issue is still vague, start with how to figure out what is wrong in your business. If the problem is already expensive, use Business Owner Coaching. The point is not to buy more motion. The point is to stop fixing the wrong thing.

Recommended next

Next step Business Owner Coaching For an expensive problem where you still do not know the next business move. Before a project Business Coaching vs Consulting Project Use this before turning an unclear problem into a bigger engagement. Business coaching hub What Business Area Needs Attention With My Business? A practical map for separating the visible problem from the real problem.